In early December, the Stockholm International Peace Research Institute (SIPRI) released a report on global arms transfers for 2020. The report states that the top 100 defense industry firms generated a combined revenue of $531 billion from arms sales and military services, a figure that is 1.3 percent higher compared with the previous year. It is worth noting that the arms sales of the top 100 defense firms in 2020 were 17 percent higher than in 2015. This means that the growth of arms sales has been steady for the past six years.

From a macro perspective, the findings of the report with regards to the growth of the sector and the steady increase in revenues are significant, especially in light of the economic and industrial instabilities resulting from the COVID-19 pandemic. Given the fact that the global economy suffered a contraction of 3.1 percent last year, this increase is even more significant.

The increase is also seen in total military spending. According to the SIPRI Yearbook 2021, world military expenditure is estimated to have been $1.981 trillion in 2020. This figure is 2.6 percent higher than in 2019 and 9.3 percent higher than in 2011. The share of military spending in world gross domestic product (GDP) increased from 2.2 percent in 2019 to 2.4 percent in 2020. The report underlines that this is the biggest increase in military burden since the global financial and economic crisis in 2009.

Trends and outlook in the arms industry

The United States continues to lead the defense market, with 41 companies being in the top 100 list. In 2020, US defense contractors generated a revenue of $285 billion. The US is followed by China, with five companies on the list and a 13 percent share of the defense market. China exported $66.8 billion of arms in 2020, a 1.5 percent increase compared to the previous year. The increase in China’s arms exports is noteworthy, especially in African and Asian markets. China offers a lucrative alternative to European and US companies by providing modern systems with a relatively low cost and no political conditions.

European companies have a 21 percent share of the global arms market with a total of $109 billion in sales. The UK and France lead the European defense sector with seven and six companies, respectively. France has made an impressive sprint recently with a sharp increase in exports to the Middle East.

The Russian market share continues to decline. In 2020, Russian companies in the Top 100 list accumulated $26.4 billion in revenues, a 6.5 percent decline compared to the previous year. The downward trend started in 2017. Problems in the Russian economy impacted the state armament program and the effects of the COVID-19 pandemic further contributed to the decrease in sales. According to SIPRI, another major factor in the negative trend is the effort by Russian defense companies to diversify their products and services to include civilian sectors. The Russian government policy aims to increase the civilian sales of the defense sector to 30 percent of total sales by 2025 and 50 percent by 2030.

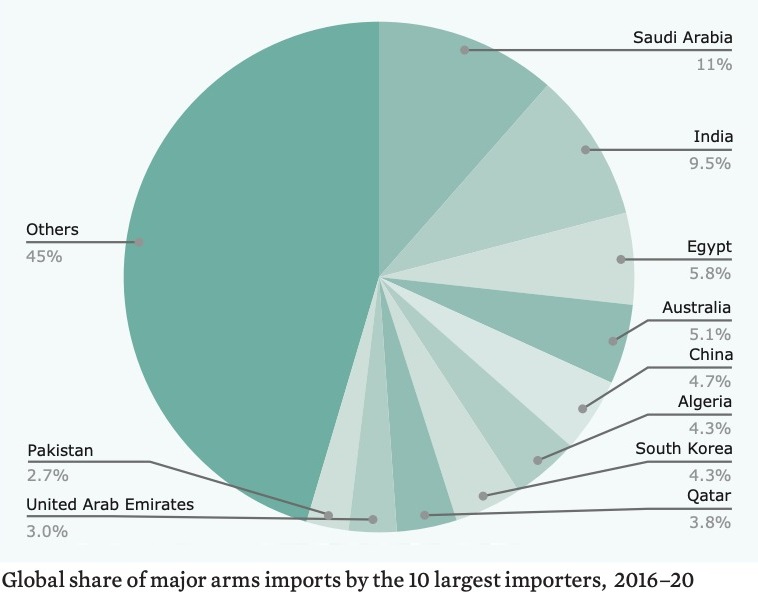

Armament in the Middle East

According to SIPRI data, Middle Eastern states were the leading customers in the global arms market in 2020. The Middle East imported 25 percent more arms in the period of 2016-2020 compared to the period of 2011-2015. Conflicts in Libya, Syria, and Yemen, as well as regional competition, have contributed to this hike in defense spending. States like Saudi Arabia, Egypt, Qatar, and the United Arab Emirates (UAE) have been the top importers.

Saudi Arabia, The United Arab Emirates (UAE), and Egypt are the three top spenders in the region. Saudi Arabia increased arms imports by 61 percent and Egypt by 136 percent in the five-year period between 2016-2020 compared to 2011-2015. But Qatar outpaced these states in terms of an increase in arms spending with a 361 percent boost. This significant figure is the result of Qatar’s disputes with other Gulf states.

After the coup in 2013, the new regime in Egypt started an extensive modernization program for the armed forces, motivated mainly by the country’s goal of becoming a regional power. Furthermore, regional competition with Turkey resulted in the allocation of more resources to the Egyptian Navy, which has taken a far lower share of arms spending compared with the air force and navy. Egypt has been modernizing the navy with the procurement of two Mistral-class amphibious assault ships, which were originally built for Russia by France but not delivered as a result of the annexation of Crimea; Type 209/1400 class submarines and MEKO A200 class frigates from Germany; FREMM class frigates and GOWIND class corvettes from France. The other major recipient of modern platforms is the Egyptian Air Force, which received a significant boost with a total of 54 Rafale jets from France and 46 MiG-29M’s from Russia.

Rafale combat aircraft have achieved remarkable export success in the Middle East recently. Egypt was the first export customer of the French-made jet, followed by Greece and Qatar, which ordered 24 Rafales in 2015 and a further 12 aircraft in 2017. Rafale’s most recent achievement is the order by the UAE in December 2021 for 80 jets worth €16 billion. The UAE order covers a large package of weapons and logistics support.

Source: SIPRI Arms Transfers Database, March 15, 2021

The UAE has been in talks with the US for the acquisition of the F-35 Lightning II 5th generation combat aircraft, and during the last days of the Trump administration, the Foreign Military Sales (FMS) process was initiated. The $23 billion deal covered 50 F-35A jets, a large precision-guided weapons package for the aircraft, and MQ-9 Reaper armed drones. The Biden administration briefly stalled the process for a review, only to resume it shortly thereafter. However, the UAE formally informed the US of a withdrawal from the talks, protesting Washington’s conditions on operations and logistics of the aircraft. The cancellation of the multi-billion-dollar deal might be a window of opportunity for other major arms suppliers to the UAE, such as France and Russia to offer alternatives. It is worth mentioning that during the Dubai Air Show 2021 in November, Russia presented two of its latest combat aircraft designs, namely the Su-57 and the new T-75 “Checkmate” by Sukhoi. Sukhoi advertises the T-75 as a direct competitor to the F-35 in the international market.

The situation in the Asia – Pacific

For the past few years, the geopolitical center of gravity has shifted to the East, specifically to the Asia-Pacific. The emergence of China as a competitor to the US has an impact on many regional developments and competitions. China’s remarkable efforts in the expansion of air and naval forces as well as flexing muscles in electronic, cyber, and missile warfare capabilities have triggered states in the region, such as Australia, South Korea, and Japan, to allocate more resources to armament. These states have become major recipients of US arms and technologies, and this regional alliance manifests itself in the acquisition of the F-35 combat aircraft.

North Korea’s and China’s missile arsenals, as well as ambitious missile development projects, will likely continue to be major factors in the armament programs of regional states. South Korea, Japan, and Australia have invested in acquiring advanced air and missile defense systems from the US, namely the AEGIS air and missile defense command and control system for use on board air defense destroyers and SM-3 and SM-6 air defense missiles. The F-35 will act as the tip of the spear of this integrated, interoperable air defense network.

India, another rival of China, has developed closer relations with the US and has begun procuring advanced platforms such as AH-64E Guardian attack helicopters, P-8I Neptune maritime patrol aircraft, and C-17 strategic transport aircraft. The US is offering an advanced version of the F-16 combat aircraft, designated F-21, to India through local production. The US attaches so much importance to enhancing strategic relations with India that Washington is expected to exempt New Delhi from the Countering America’s Adversaries Through Sanctions Act (CAATSA) for purchasing S-400 air defense systems from Russia.

In conclusion, the Middle East and Asia-Pacific will dominate the arms market for the coming years. China’s regional and global ambitions will likely result in more spending by its competitors and the US on advanced weapons, whereas ongoing conflicts and regional competition will sustain the Middle East’s position in the global arms market.